by Eric Marshall, CFA, on Jul 17, 2026

Stock prices ultimately follow earnings” – Bill Berger

In 2Q26, U.S. equities delivered a powerful rebound as earnings momentum seemed to overshadow military actions in Iran, oil price worries, and policy uncertainty surrounding the new leadership at the Federal Reserve. The S&P 500 finished the quarter up 15.2%, and small-cap stocks, as measured by the Russell 2000, gained over 21%. This marked the eighth-best quarterly performance for the Russell 2000 since its inception in the 1970s. As concerns eased about private credit and a potential AI-driven shock to employment, leadership broadened during the recent quarter. While technology and AI-related companies continued to lead overall returns, we saw a healthy rotation into economically sensitive sectors such as industrials and financials as confidence in the economic outlook improved. Investors also warmed up to healthcare-related stocks in 2Q26. The primary laggards included energy, communication services, and consumer discretionary.

PE multiples for the most part remained flat this year as an improved outlook for earnings expectations held up amid a more uncertain economic backdrop for inflation and interest rates. While forward PE multiples saw little change in 2Q26, expectations for earnings growth accelerated in response to solid economic activity across many industrial sectors that have had to adapt to global economic uncertainty, inflation, and a higher cost of capital over the past few years. Growth expectations for S&P 500 earnings were a solid 18.8% at the beginning of 2Q26 and rose to 23.3% by the end of the quarter. Corporate profit margins have generally expanded in recent months, supporting a positive outlook for this year and next. After several years of underperformance, the growth trajectory of small-cap earnings (based on S&P 600 Bloomberg consensus data) now exceeds the earnings growth expectations for the S&P 500. Over the next 12 months, industry analysts collectively project 17% earnings growth for the S&P 500 and more than 19% for the S&P 600. According to FactSet data, the 12-month forward PE multiple for the S&P 500 is now 20.4X, down from 22.2X at the start of the year and 19.9X at the end of March. The inverse of the current S&P 500 PE multiple is a forward earnings yield of 4.9%, which is above the year-end 10-year Treasury yield of 4.5%. This comparison suggests that equity valuations are somewhere between reasonable and slightly attractive, assuming the upward trend in earnings estimates materializes in the back half of 2026 and 2027.

Our conversations with corporate leadership during the past quarter were generally constructive, reflecting improving business confidence despite uncertainty surrounding interest rates and commodity prices. Management teams also indicated that capital deployment activity has increased compared to a year ago, supporting a favorable business backdrop. These discussions reinforce our view that earnings momentum remains positive in the back half of 2026, with profit margins holding up well.

We continue to see attractive long-term investment opportunities in consumer growth companies, infrastructure development, AI-driven investment, energy innovation, and the ongoing renaissance in domestic manufacturing. We believe this dynamic environment has created compelling opportunities for active, fundamental stock selection in companies that stand to benefit from long-term structural trends and favorable sector-specific momentum. While we recognize that markets do not move higher indefinitely, we believe periodic profit-taking and leadership rotation into areas that have lagged over the past several years are both healthy for our portfolios and necessary characteristics of a sustainable bull market. We continue to find compelling opportunities in overlooked companies that stand to benefit from several long-term secular growth themes, including healthcare innovation, technology automation, and financial services. Through disciplined, fundamental research, we seek to identify businesses that are well-positioned to capitalize on these enduring megatrends while trading at attractive valuations.

At Hodges Capital, our commitment to a fundamental, research-driven investment philosophy remains steadfast. We are dedicated to uncovering opportunities in well-managed businesses that can deliver enduring value to our shareholders.Returns (% Retail Class) as of 6/30/2026

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. The current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-811-0224. The Funds impose a 1.00% redemption fee on shares held for thirty days or less (60 days or less for Institutional Class shares). Performance data quoted does not reflect the redemption fee. If reflected, total returns would be reduced. Performance reflected is net of all other fees and expenses.

Hodges Small Cap Growth Fund (HDPSX)

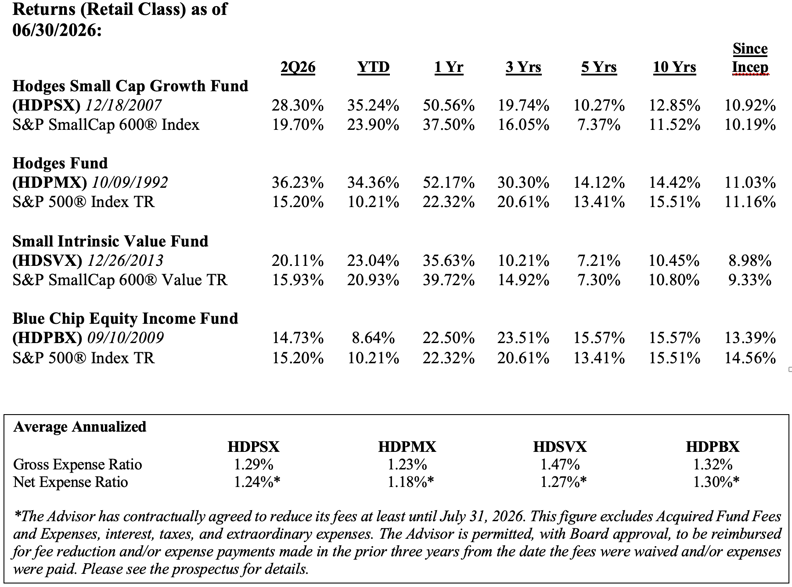

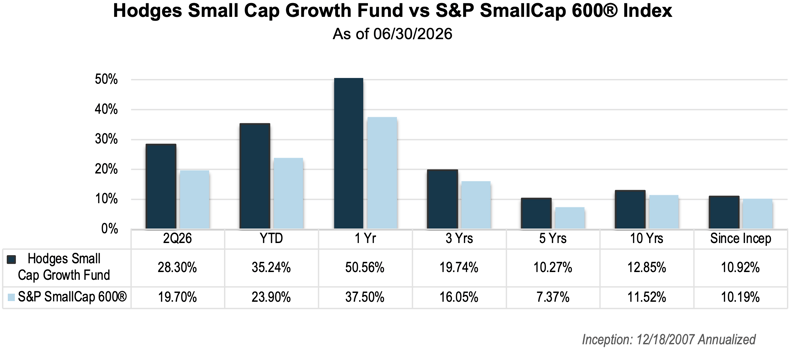

The return for the Hodges Small Cap Growth Fund amounted to a gain of 28.30% in the second quarter of 2026, compared to a 19.70% gain for the S&P SmallCap 600 Index. The Small Cap Growth Fund's 12-month return as of June 30, 2026, amounted to a gain of 50.56% compared to a gain of 37.50% for the S&P SmallCap 600 Index during the same period. Outperformance in the recent quarter reflected the fund's exposure to industrial, infrastructure, and semiconductor stocks, which have been the strongest contributors to the portfolio’s performance this year. Although small-cap stocks have underperformed large-cap stocks for the better part of the past decade, we still consider the current risk-reward for holding quality small-cap stocks to be attractive. While small-cap stocks tend to experience greater volatility during market turmoil, we expect this segment to deliver above-average, risk-adjusted returns over the long term. Furthermore, many small-cap companies are uniquely positioned to benefit from a pick-up in M&A activity, AI productivity enhancements, and the reshoring of manufacturing in the year ahead.

The Hodges Small Cap Growth Fund remains well diversified across industrials, financials, transportation, technology, and consumer-related names, which we expect to contribute to the Fund's long-term performance. The Fund recently took profits in several stocks that appeared overvalued relative to their underlying fundamentals and established new positions with an attractive risk/reward profile. During the recent quarter, the Fund increased its number of total positions from 44 to 48 positions as of June 30, 2026. The top ten holdings amounted to 32.37% of the Fund's holdings and included TeraWulf Inc (WULF), Matador Resources (MTDR), Eagle Materials Inc (EXP), DigitalOcean Holdings Inc (DOCN), Maxlinear Inc (MXL), Banc of California Inc (BANC), Texas Pacific Land Corporation (TPL), Texas Cap Bancshares Inc (TCBI), Clear Secure Inc (YOU), and Geo Group Inc (GEO).

Hodges Fund (HDPMX)

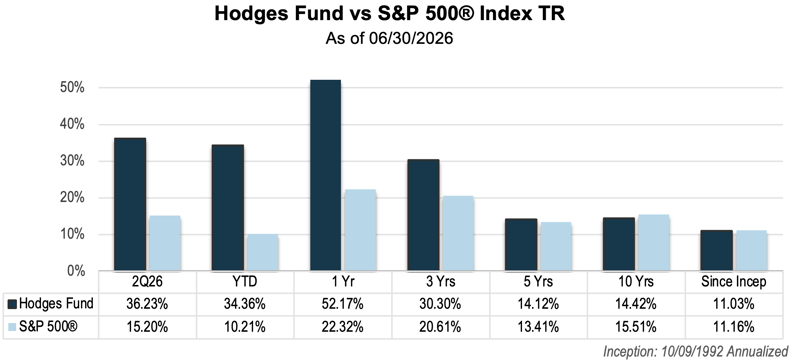

The return for the Hodges Fund amounted to a gain of 36.23% in the second quarter of 2026, compared to a 15.20% gain for the S&P 500 Index. The Fund’s 1-year performance generated a return of 52.17%, outperforming the S&P 500's 22.32%. This performance reflects strength in individual holdings within a concentrated portfolio, with several top holdings more than doubling over the past twelve months, including Terawulf (WULF), Carpenter Technologies (CRS), Vishay Precision Group Inc (VPG), and Micron Technologies (MU). Elevated portfolio turnover enabled timely updates to holdings, targeting companies with above-average return potential relative to downside risks over the next 12 to 18 months.

The Hodges Fund's portfolio managers remain focused on investments with the highest conviction, based on fundamentals and relative valuations. The number of positions held in the Fund at the end of the recent quarter was 40. As of June 30, 2026, the top ten holdings accounted for 47.14% of the Fund's assets. They included Micron Technology Inc (MU), Terawulf Inc (WULF), SharkNinja, Inc. (SN), Applied Materials Inc (AMAT), Texas Pacific Land Corporation (TPL), Uber Technologies (UBER), Vishay Precision Group Inc (VPG), Viking Holdings Ltd (VIK), Freeport-McMoRan (FCX) and DraftKings Inc. (DKNG).

Hodges Small Intrinsic Value Fund (HDSVX)

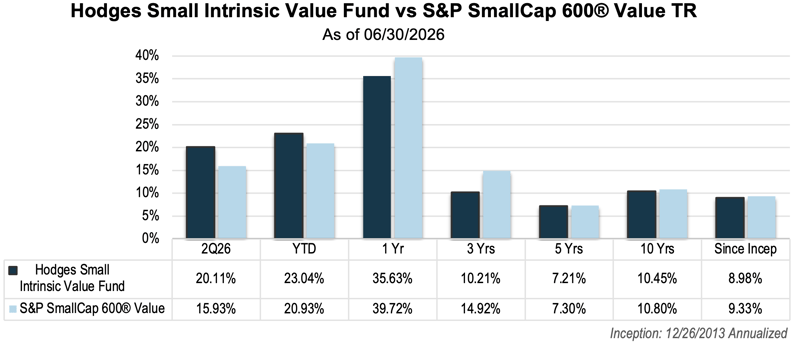

The Hodges Small Intrinsic Value Fund experienced a gain of 20.11% in the second quarter of 2026 compared to an increase of 15.93% for its benchmark, S&P SmallCap 600 Value Index. The Small Intrinsic Value Fund's 1-year performance as of June 30, 2026, amounted to a gain of 35.63% compared to an increase of 39.72% for the S&P SmallCap 600 Value Index during the same period. The Fund's outperformance in the second quarter reflected above-average performance among several of its semiconductor and industrially related names. The number of positions held in the Fund at the end of the recent quarter was 47. As of June 30, 2026, the top holdings represented 32.99% of the Fund's assets. They included Academy Sports & Outdoors (ASO), Garrett Motion Inc (GTX), Powell Industries Inc (POWL), Banc of California Inc (BANC), Eagle Materials Inc (EXP), Geo Group Inc (GEO), Texas Capital Bancshares (TCBI), Triumph Financial Inc (TFIN), Maxlinear Inc (MXL) and Ryman Hospitality Properties Inc (RHP).

Hodges Blue Chip Equity Income Fund (HDPBX)

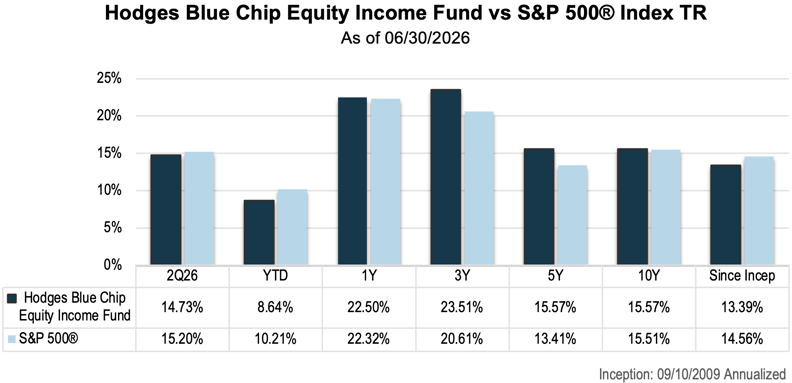

The Hodges Blue Chip Equity Income Fund experienced a gain of 14.73% in the second quarter of 2026, compared to a gain of 15.20% for its benchmark, the S&P 500 Index. The Blue Chip Fund's 1-year performance as of June 30, 2026, amounted to a gain of 22.50%, compared to an increase of 22.32% for the S&P 500 Index during the same period. We believe the current investment landscape offers ample opportunities among high-quality, dividend-paying stocks with solid upside potential. We expect underleveraged balance sheets and robust corporate profits across most blue-chip stocks to support stable dividend yields over the next several years. The Blue Chip Equity Income Fund remains well-diversified in companies that we believe can generate above-average income and total returns on a risk-adjusted basis. The Fund held 29 positions at the end of the recent quarter. The top ten holdings at the end of the quarter represented 45.74% of the Fund's holdings and included Nvidia (NVDA), Broadcom Inc (AVGO), Eli Lilly & Co (LLY), Apple Inc (AAPL), Taiwan Semiconductor (TSM), Walmart Inc (WMT), Boeing Co (BA), Citigroup Inc (C), Goldman Sachs Group Inc (GS) and Microsoft Corp (MSFT).

In conclusion, we remain optimistic about the long-term investment opportunities surrounding the Hodges Mutual Funds. With four distinct mutual fund strategies that cover most segments of the domestic equity market, we are well-positioned to meet the diverse needs of financial advisors and individual investors. Our dedicated investment team continues to rigorously analyze companies, engage with management teams, and monitor market trends to navigate the ever-changing economic landscape. If you have any specific questions, please don't hesitate to contact us directly .

Learn more about Hodges Funds:

|

|

|||

|

|

The above discussion is based on the opinions of Eric Marshall, CFA, and is subject to change. It is not intended to be a forecast of future events, a guarantee of future results, and is not a recommendation to buy or sell any security. Portfolio composition and company ownership in the Hodges Funds are subject to daily change.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory and summary prospectuses contain this and other important information about the Hodges Funds, and it may be obtained by calling 866-811-0224, or visiting hodgescapital.com/mutual-funds. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. Options and future contracts have the risks of unlimited losses of the underlying holdings due to unanticipated market movements and failure to correctly predict the direction of securities prices, interest rates and currency exchange rates. These risks may be greater than risks associated with more traditional investments. Short sales of securities involve the risk that losses may exceed the original amount invested. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer term debt securities. Investments in small and medium capitalization companies involve additional risks such as limited liquidity and greater volatility. Funds that are non-diversified are more exposed to individual stock volatility than a diversified fund. Investments in companies that demonstrate special situations or turnarounds, meaning companies that have experienced significant business problems but are believed to have favorable prospects for recovery, involve greater risk.

Value investing carries the risk that the market will not recognize a security’s inherent value for a long time, or that a stock judged to be undervalued may be appropriately priced or overvalued.

Diversification does not assure a profit or protect against a loss in a declining market.

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

The S&P 500 Index is a broad-based unmanaged index of 500 stocks that is widely recognized as representative of the equity market in general. The Russell 1000 Total Return Index is a subset of the Russell 3000 Index and consists of the 1,000 largest companies comprising over 90% of the total market capitalization of all listed stocks. The Russell 2000 Index consists of the smallest 2,000 companies in a group of 3,000 US companies in the Russell 3000 Index, as ranked by market capitalization. The Russell 2500 Index consists of the smallest 2,500 companies in a group of 3,000 US companies in the Russell 3000 Index, as ranked by market capitalization. The Russell 3000 Index is a stock index consisting of the 3000 largest publicly listed companies, representing about 98% of the total capitalization of the entire US stock market. You cannot invest directly in an index. The Russell 2000 Value Index measures the performance of the small-cap value segment of the US equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Value Index is constructed to provide a comprehensive and unbiased barometer for the small-cap value segment. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set and that the represented companies continue to reflect value characteristics.

Cash Flow: A revenue or expense stream that changes a cash account over a given period.

Price/earnings (P/E): The most common measure of how expensive a stock is.

Earnings Growth is not a measure of the Fund’s future performance.

Hodges Capital Management is the Advisor to the Hodges Funds.

The Hodges Funds are distributed by Northern Lights Distributors, LLC.