by Eric Marshall, CFA, on Jan 19, 2023

“If you wait for someone to ring a bell or blow a whistle before you invest, it’s too late.” – Monte Gordon

U.S. stocks staged a comeback in the fourth quarter of 2022, with the S&P 500 increasing by 7.6% to close the year down 18.1%. The NASDAQ Composite was down 0.8% in the quarter to finish the year down 33.0%, reflecting the worst performance for the tech-heavy index since 2008. As measured by the Russell 2000, Small-caps rose 6.2% in the year's final quarter, resulting in a decline of 20.4% in 2022. Value continued to outpace growth in the year's final quarter as global economic uncertainty overshadowed worries over inflation in the face of the fastest pace of Fed rate hikes in forty years. As a result, Price/earnings (P/E) multiples contracted throughout 2022 to adjust to the reality of higher interest rates and the likelihood of an earnings recession in the year ahead. While the recent turbulence in financial markets has been unsettling, three of the four Hodges Mutual Funds generated positive 2022 returns relative to their respective benchmarks. Although broad repricing of most risk assets resulted in few places to hide in 2022, our focus on companies with sound business fundamentals and reasonable valuations contributed to positive relative performance in several fund strategies.

As we look back on the turmoil of 2022, capital markets may have already priced in uncertainty regarding the trajectory of interest rates and the prospects for changing economic conditions in 2023. In our opinion, the year-to-date sell-off has priced a slowdown in the global economy next year and an appropriate contraction in PE multiples relative to current interest rates. According to the most recent data published by FactSet, the S&P 500 is trading at approximately 17.3X forward earnings estimates compared to 21.2X at the beginning of 2022 and the five-year average of 18.5X. Although PE multiples have contracted, the inverse of the S&P 500 quarter-end PE multiple reflected an earnings yield of 5.78%, which was still above the 10-year Treasury yield of 3.88% at year-end. The big macro questions are now; How much will the global economy slow next year, and to what degree will it drag on corporate earnings and cash flow? We would argue that an economic slowdown in 2023 could be the most anticipated recession in the past forty years. As a result, many businesses have spent a good deal of the past year cutting costs, scrutinizing capital expenditures, tightening supply chains, and cautiously managing inventories. In theory, the more a recession is anticipated, the greater the likelihood a downturn could be shallow as businesses quickly avoid building excess capacity and inventories. Our investment team's recent discussions with public company management teams over the past months suggest that labor costs are stabilizing, and many other input costs have begun to moderate in recent months. Consumer spending increased in 2022 due to excess savings built up during the pandemic but appears less certain heading into 2023. The housing market has cooled down due to thirty-year mortgage rates rising from 3.1% to a peak of 7.1% and finishing the year at 6.4%. Manufacturing is undergoing a renaissance due to onshoring and nearshoring supply chains, a trend likely to continue in 2023. Companies with meaningful exposure to the Eurozone seem the most susceptible to a global recession in the year ahead. However, not every economic slowdown looks the same, and not every business will be affected the same by potential macro headwinds. In this environment, we believe active portfolio management becomes essential to navigate quickly changing business conditions across many sectors. Furthermore, a slowdown in the economy and higher interest rates favored stocks with solid balance sheets whose underlying assets has produced stable cash flow and earnings. Although the market is pricing in a more challenging macro environment for earnings in the balance of the year, we still see opportunities in stocks that potentially have the staying power to deal with volatile prices and curtailed discretionary spending. Challenging macro conditions and the recent sell-off in stock prices will likely result in new sector leadership in the months ahead. With this in mind, the Hodges Capital Management investment team has positioned our portfolios with the goal to benefit from shifting economic trends and secular and structural changes across different industries.

As we gaze into the widely anticipated economic abyss of 2023, our portfolios remain laser-focused on fundamental investing and individual stock selection. Our investing approach involves spending no time predicting short-term fluctuations in interest rates, foreign currencies, or commodity prices. Instead, we pay close attention to how prices and, more importantly, the pricing power that our portfolio companies exhibit within the goods and services they produce. For many businesses, inflation and a slowdown in demand could adversely impact profit margins and revenues in the months ahead. Companies that exhibit pricing power and a low threat from substitute products can often pass on higher costs and potentially see profit margins benefit even in a challenging economic environment. As a result, we are overweighting our portfolios with growth and value stocks that we believe can create shareholder value despite challenging macro conditions.

There is no shortage of worrisome macro headlines and economic uncertainty as we attempt to capitalize on lower year-over-year stock prices. What we know for sure is what we do not know. We do not know the day that the bear market will bottom, the peak level of interest rates, or the exact severity of an economic slowdown in 2023. We do know that investor sentiment is generally negative, and the P/E multiples for the Russell 2000 and S&P 500 have contracted to reflect higher interest rates and earnings uncertainty. Specific sectors of U.S. stocks, such as housing, transportation, retail, semiconductors, and other cyclicals, appear to have priced in a meaningful slowdown in the months ahead. The lack of capital flows into equities, and overall cash levels indicate that investors are defensively positioning portfolios, which is part of the bottoming process for any bear market. The big question in the coming months is: What will investors be willing to pay for future earnings in a rising interest rate environment, and what earnings expectations are priced into individual stock prices? We believe the PE multiple for the broader market has adjusted appropriately to the current interest rate environment. However, this is not true for every stock, as we see the potential to unlock value for many under-the-radar companies in our portfolios.

During this time of ambiguity, the investment team at Hodges Capital is rigorously looking for bargains in businesses that we believe are well-run and control their destiny by relying on ingenuity and well-calculated business decisions rather than day-to-day momentum in the stock market. Investors in the Hodges Funds can be assured that we are not changing our core investment discipline, designed to seek out quality companies running great businesses with excellent management teams trading at reasonable prices. Furthermore, we see this as an ideal environment for active portfolio managers to carefully select individual stocks that we believe can generate long-term value for shareholders.

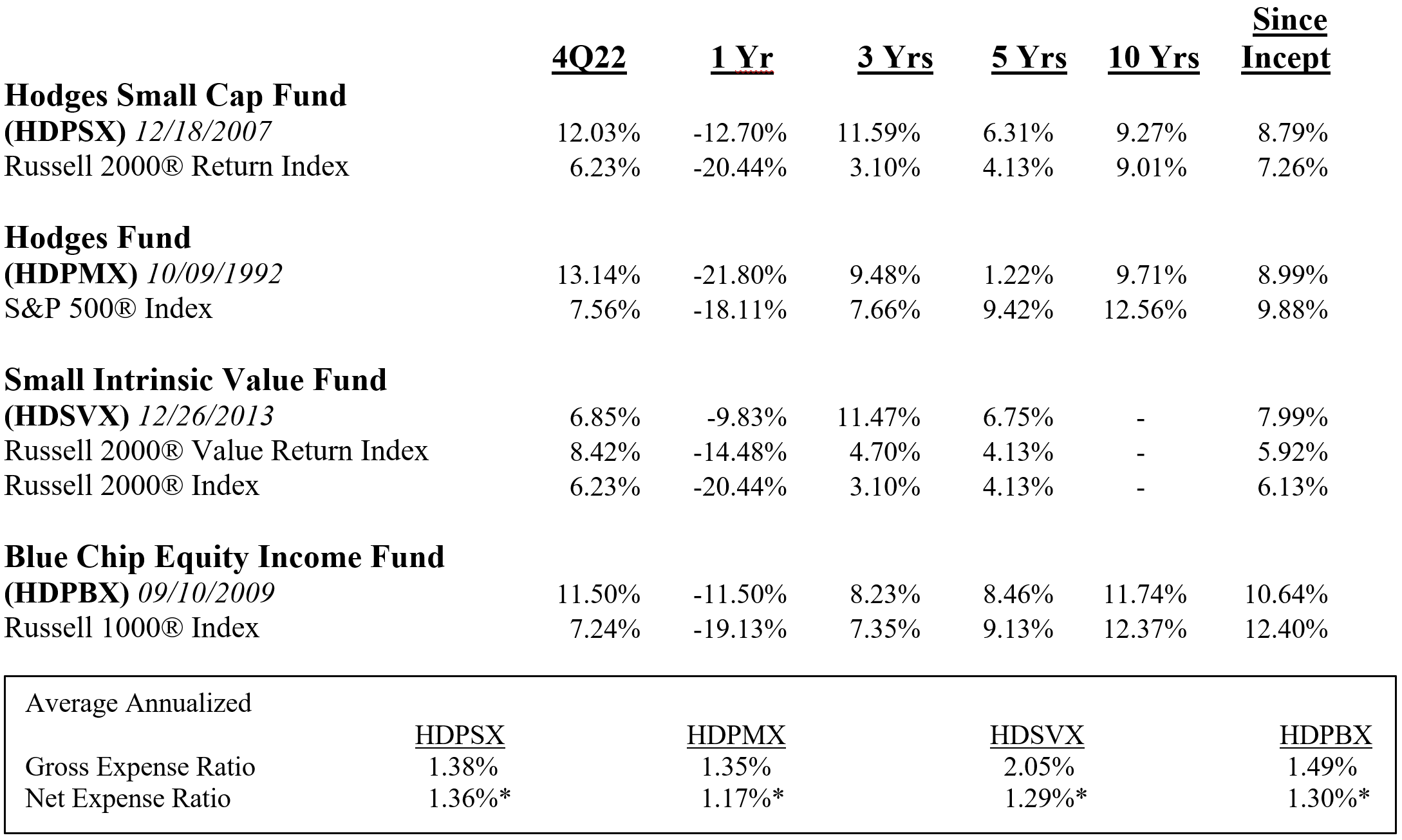

Returns (% Retail Class) as of 12/31/2022

*The Advisor has contractually agreed to reduce its fees at least until July 31, 2023. This figure excludes Acquired Fund Fees and Expenses, interest, taxes, and extraordinary expenses. The Advisor is permitted, with Board approval, to be reimbursed for fee reduction and/or expense payments made in the prior three years from the date the fees were waived and/or expenses were paid. Please see prospectus for details.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. The current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-811-0224. The Funds impose a 1.00% redemption fee on shares held for thirty days or less (60 days or less for Institutional Class shares). Performance data quoted does not reflect the redemption fee. If reflected, total returns would be reduced.

Hodges Small Cap Fund (HDPSX)

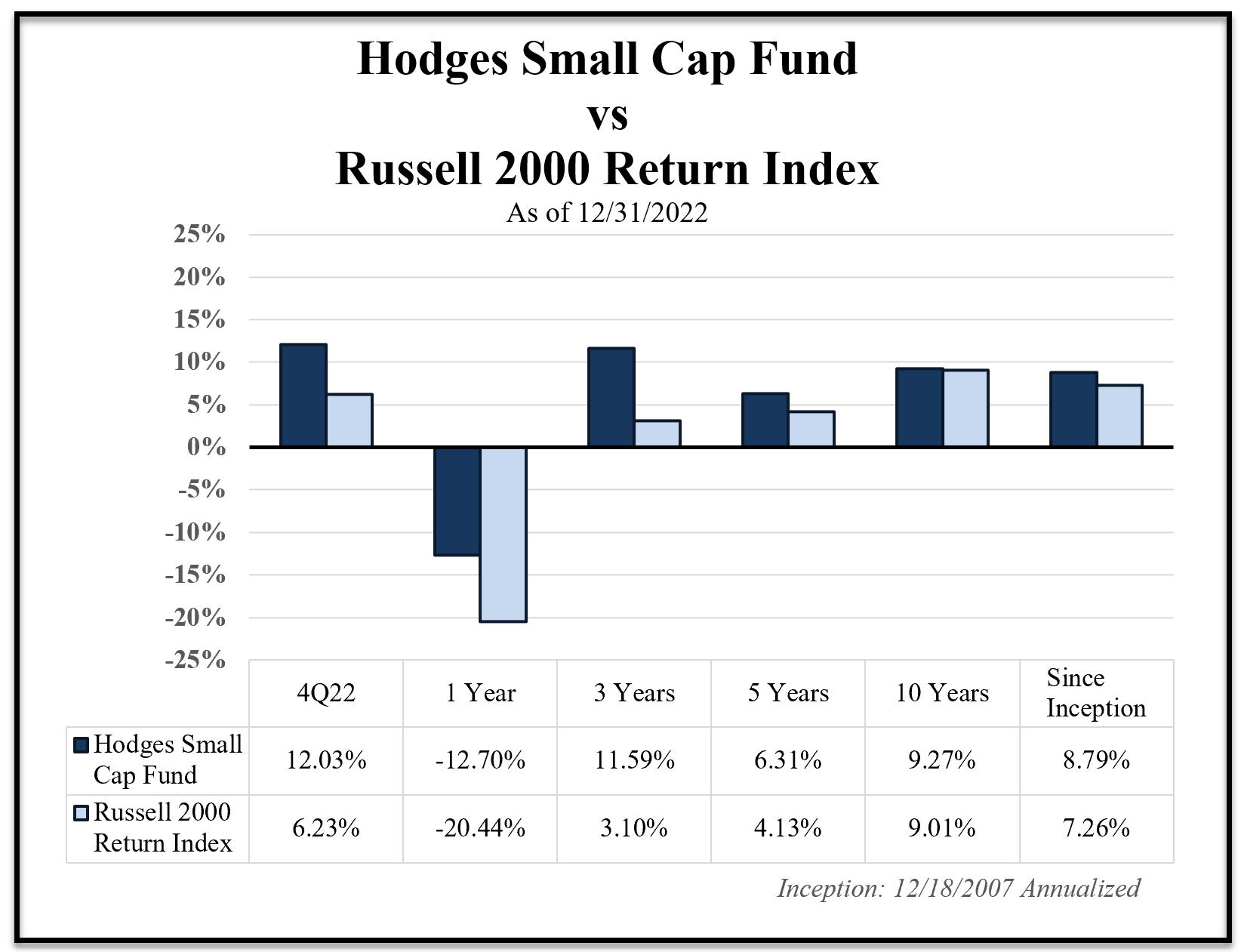

The return for the Hodges Small Cap Fund amounted to a gain of 12.03% in 4Q22 compared to an increase of 6.23% for the Russell 2000 Index. The Fund's 2022 return amounted to a loss of 12.70% compared to a loss of 20.44% for the Russell 2000 Index during the same period. Although small-caps have been underperforming large-cap stocks this year, we view the current risk-reward for holding quality small-cap stocks as attractive. While small-cap stocks tend to experience greater volatility during a period of market turmoil, we anticipate this segment to generate above-average relative risk-adjusted returns over the long term.

The Hodges Small Cap Fund remains well diversified across industrials, transportation, financial services, technology, and consumer-related names, which we expect to contribute to the Fund's long-term performance. The Fund recently took profits in several stocks that appeared overvalued relative to their underlying fundamentals and established several new positions with an attractive risk/reward profile. The Fund had a total of 50 positions at December 31, 2022. The top ten holdings amounted to 38.89% of the Fund's holdings and included Matador Resources (MTDR), SM Energy Co (SM), Texas Pacific Land Corp (TPL), Eagle Materials Inc (EXP), Commercial Metals Co (CMC), Taylor Morrison Home Corp (TMHC), Hilltop Holdings Inc (HTH), Cleveland-Cliffs Inc (CLF), Encore Wire Corp (WIRE), and Inmode Ltd (INMD).

Hodges Small Cap Fund vs Russell 2000 Return Index

Hodges Fund (HDPMX)

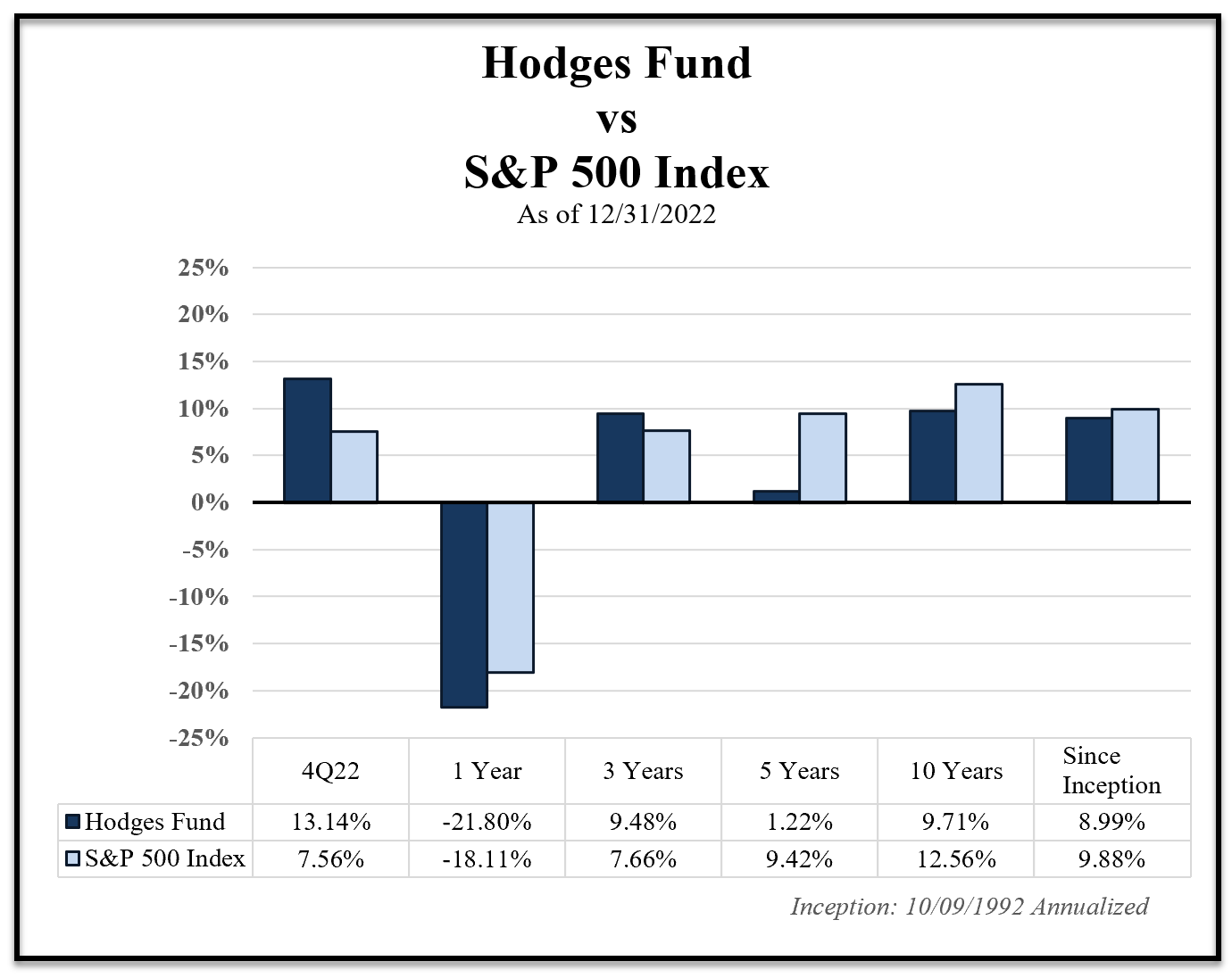

The Hodges Fund's fourth quarter of 2022 return amounted to a gain of 13.14% compared to an increase of 7.56% for the S&P 500 Index. For the year, the Fund returned a loss of 21.80%, compared to a loss of 18.11% for the S&P 500 Index. In the recent quarter, improved relative performance was attributed to a handful of consumer discretionary and energy stocks that held up well in the recent quarter. The Hodges Fund’s turnover has recently picked up to take advantage of volatile market conditions. We have upgraded many portfolio holdings into stocks that we believe offer above-average returns relative to their downside risks over the next twelve to eighteen months.

While we were disappointed with the Fund's underperformance in 2022, the Hodges Fund's portfolio managers remain laser-focused on investments where we have the highest conviction based on fundamentals and relative valuations. The number of positions held in the Fund at the end of the recent quarter increased from 35 to 40. On December 31, 2022, the top ten holdings represented 49.47% of the Fund's holdings. They included Texas Pacific Land Corp (TPL), Matador Resources Co (MTDR), Encore Wire Corp (WIRE), Chesapeake Energy Corp (CHK), On Semiconductor (ON), Uber Technologies (UBER), Cleveland-Cliffs Inc (CLF), Topgolf Callaway Brands (MODG), On Holdings (ONON), and General Motors Co (GM).

Hodges Fund vs S&P 500 Index

Hodges Small Intrinsic Value Fund (HDSVX)

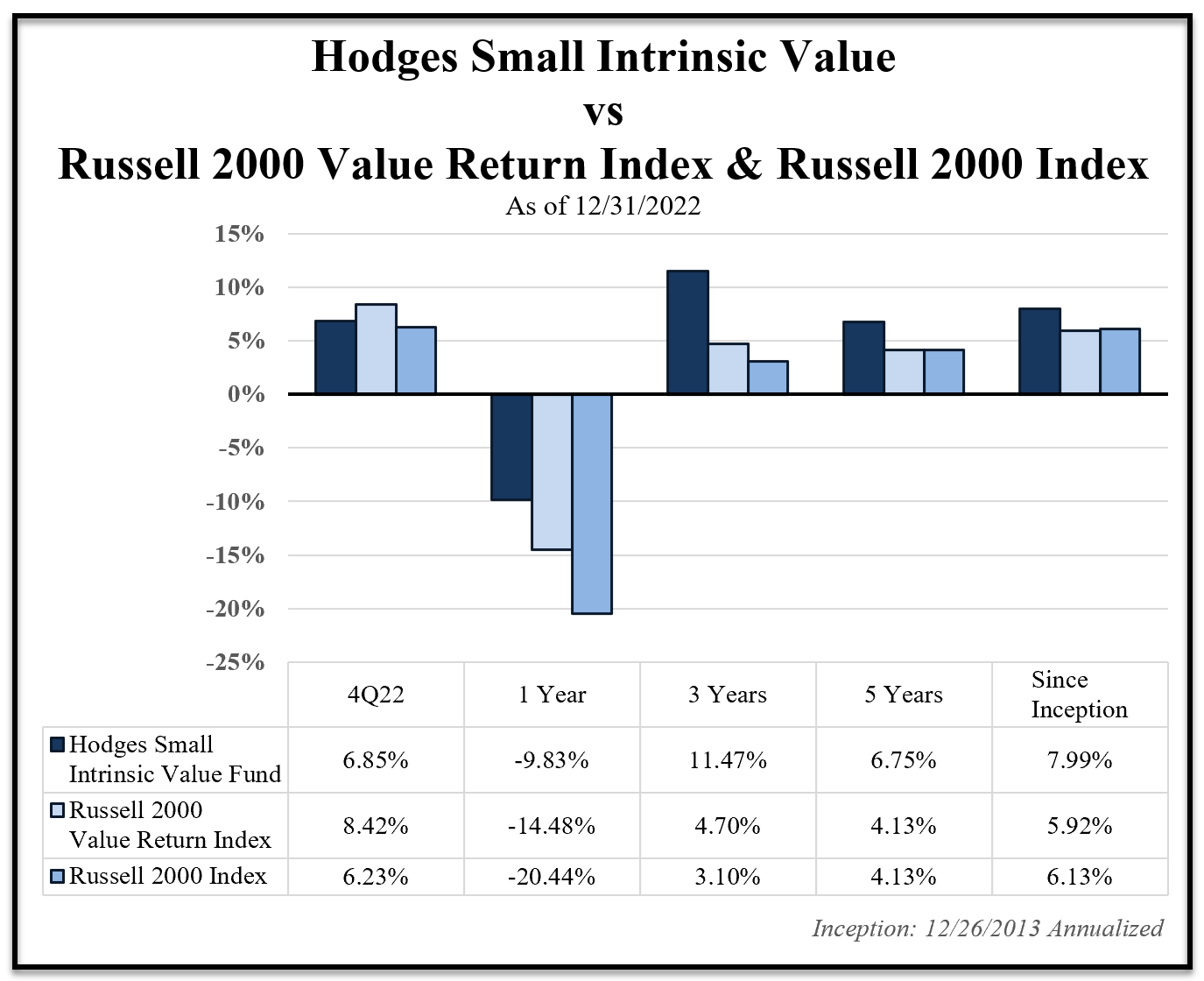

The Hodges Small Intrinsic Value Fund experienced a gain of 6.85% in the fourth quarter of 2022 compared to a gain of 8.42% for its benchmark, the Russell 2000 Value Index. The year-to-date return for 2022 amounted to a loss of 9.83% compared to a loss of 14.48% return for the Russell 2000 Value Index. The Fund's solid relative performance over the past year was attributed to several of the Fund's energy, material, consumer stables, and industrial stocks. The Fund increased its positions from 4DD2 to 46 for the quarter ending December 31, 2022. The top holdings represented 33.87% of the Fund's holdings and included Eagle Materials Inc (EXP), Vista Outdoor Inc (VSTO), Triumph Financial Inc (TFIN), Chesapeake Energy Corp (CHK), Texas Capital Bancshares (TCBI), Propetro Holding Corp (PUMP), Chord Energy Corp (CHRD), Home Bancshares Inc (HOMB), and Treehouse Foods Inc (THS).

Hodges Small Intrinsic Value Fund vs Russell 2000 Value Return Index & Russell 2000 Index

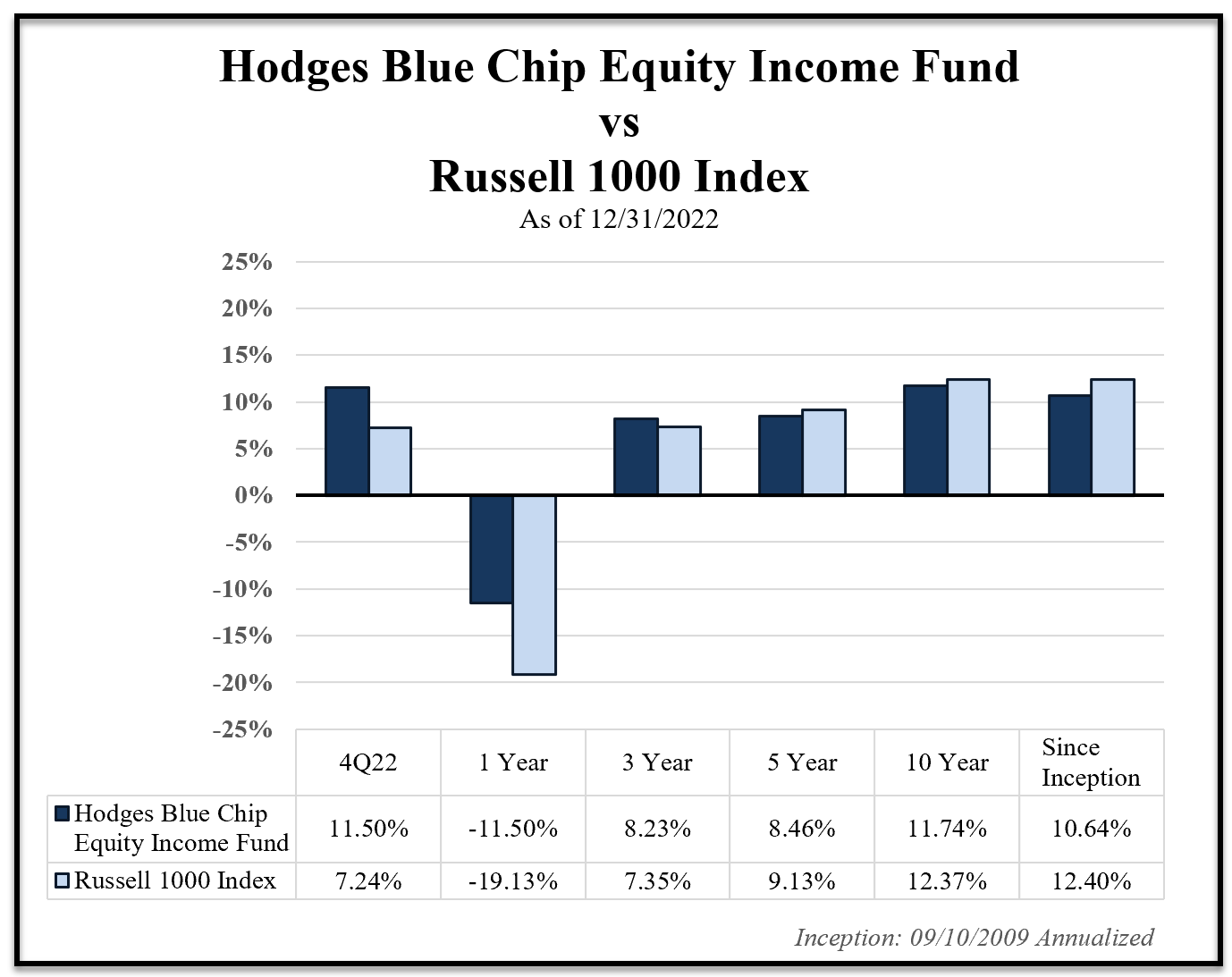

Hodges Blue Chip Equity Income Fund (HDPBX)

The Hodges Blue Chip Equity Income Fund was up 11.5% in the December Quarter of 2022, compared to a gain of 7.24% for the Russell 1000 Index. The Fund experienced a negative return of 11.5% compared to a loss of 19.13% for the Russell 1000 Index in 2022. Positive relative performance in the recent quarter was attributed to stock selection among a handful of the energy and technology names. Although large-cap stocks have held up better than small and mid-cap stocks during the recent sell-off, we see the current investing landscape as offering plenty of attractive, high-quality dividend-paying stocks with solid upside potential. We expect underleveraged balance sheets and corporate profits across most blue-chip stocks to support stable dividends over the next several years. The Blue Chip Equity Income Fund remains well-diversified in companies that we believe could generate above-average income and total returns on a risk-adjusted basis. The Fund had a total of 30 positions at December 31, 2022. The top ten holdings at the end of the quarter represented 51.00% of the Fund's holdings and included Deere & Co (DE), Exxon Mobil Corp (XOM), Apple Inc (AAPL), Microsoft Corp (MSFT), Caterpillar Inc (CAT), Pepsico Inc (PEP), Home Depot Inc (HD), Texas Instruments Inc (TXN), Oneok Inc (OKE), and Johnson & Johnson (JNJ).

Hodges Blue Chip Equity Income Fund vs Russell 1000 Index

In conclusion, we remain optimistic regarding the long-term investment opportunities surrounding the Hodges Mutual Funds. By offering four distinct mutual fund strategies covering most segments of the domestic equity market, we can serve most financial advisors' and individual investors' diverse needs. Our entire investment team is rigorously studying companies, meeting with management teams, observing trends, and navigating today's ever-changing financial markets. Feel free to contact us directly if we can address any specific questions.

Learn more about Hodges Funds:

|

|

|||

|

|

The above discussion is based on the opinions of Eric Marshall, CFA, and is subject to change. It is not intended to be a forecast of future events, a guarantee of future results, and is not a recommendation to buy or sell any security. Portfolio composition and company ownership in the Hodges Funds are subject to daily change.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory and summary prospectuses contain this and other important information about the Hodges Funds, and it may be obtained by calling 866-811-0224, or visiting www.hodgesmutualfunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. Options and future contracts have the risks of unlimited losses of the underlying holdings due to unanticipated market movements and failure to correctly predict the direction of securities prices, interest rates and currency exchange rates. These risks may be greater than risks associated with more traditional investments. Short sales of securities involve the risk that losses may exceed the original amount invested. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer term debt securities. Investments in small and medium capitalization companies involve additional risks such as limited liquidity and greater volatility. Funds that are non-diversified are more exposed to individual stock volatility than a diversified fund. Investments in companies that demonstrate special situations or turnarounds, meaning companies that have experienced significant business problems but are believed to have favorable prospects for recovery, involve greater risk.

Value investing carries the risk that the market will not recognize a security’s inherent value for a long time, or that a stock judged to be undervalued may be appropriately priced or overvalued.

Diversification does not assure a profit or protect against a loss in a declining market.

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

The S&P 500 Index is a broad-based unmanaged index of 500 stocks that is widely recognized as representative of the equity market in general. The Russell 1000 Index is a subset of the Russell 3000 Index and consists of the 1,000 largest companies comprising over 90% of the total market capitalization of all listed stocks. The Russell 2000 Index consists of the smallest 2,000 companies in a group of 3,000 U.S. companies in the Russell 3000 Index, as ranked by market capitalization. The Russell 2500 Index consists of the smallest 2,500 companies in a group of 3,000 U.S. companies in the Russell 3000 Index, as ranked by market capitalization. The Russell 3000 Index is a stock index consisting of the 3000 largest publicly listed companies, representing about 98% of the total capitalization of the entire U.S. stock market. The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Value Index is constructed to provide a comprehensive and unbiased barometer for the small-cap value segment. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set and that the represented companies continue to reflect value characteristics. The NASDAQ Composite Index is an index of more than 3,000 common equities listed on the NASDAQ stock market. You cannot invest directly into an index.

Cash Flow: A revenue or expense stream that changes a cash account over a given period.

Price/earnings (P/E): The most common measure of how expensive a stock is.

Earnings Growth is not a measure of the Fund’s future performance.

Hodges Capital Management is the Advisor to the Hodges Funds.

Hodges Funds are distributed by Quasar Distributors LLC.