Transitioning to Fall: 4 Headlines to Monitor

by Hodges Investment Team, on September 13, 2022

As we move into fall, send our kids back to school, and ease into football season, there are some big items worth our attention. Here’s a little color.

#1: Mid-term Elections

We do not look at politics from an ideological perspective, as that would potentially invite personal bias. Rather we look at politics purely from an investment perspective. With that in mind, the mid-terms are coming, and we will soon be in the throes of the relentless advertising and mudslinging that (sadly) precedes every election. I would venture to guess that the market will continue with its wild mood swings, both up and down, until we see the outcomes, for this is what tends to happen during the heat of election years.

The Market Loves Political Gridlock

What should be noted is that in mid-term elections, the party who lost the White House two years prior, usually picks up seats in either the House, Senate, or both. Why does this happen? The loss of the Presidency tends to reinvigorate the voter base within the other party. Why is this important? If history continues, and one or both houses of congress flip from a Democrat to Republican majority, we’ll be in a state of political gridlock. The market loves gridlock because there is an extremely low probability of onerous legislation passing. The political risk (of investing) has been, therefore, largely alleviated.

Worth a reminder: Given that Build Back Better’s initial ask was $3 Trillion with numerous tax hits from all angles, and the final result (renamed the Inflation Reduction Act) was $400 Billion with only a couple of tax hits, we are already operating in quasi gridlock.

#2: Inflation/Fed/Interest Rates

We’ve all been steeping in Fed Speak since the first interest rate hike back in March. We’ve also been made acutely aware that we are paying more for pretty much everything, hence the Fed’s aggressive stance to break the caustic back of inflation. As commodity prices have skyrocketed since late 2021, recently they have started to reverse course and soften. Most of us have witnessed this at the gas pump, as prices have ebbed since the spike in early summer, but it holds true across just about every commodity price. This is a positive because commodities are inputs in that companies use them to make their end products. If companies are paying less for the inputs, we as consumers will ultimately pay less at the checkout stand. It might take several months for the pricing correction to pass through, but it seems to be going in the right direction. So, the big question here is if this recent softening will continue.

We’ll get a glimpse of that on September 13th when the August CPI is released. The next Fed meeting regarding interest rate policy will be held September 20-21, so the CPI report will most certainly be part of their analysis. As to what they will do, I wish I had a crystal ball for that answer.

#3: Russia/Ukraine

What was once an incredibly scary headline has now faded. We certainly still get snippets, but they are not nearly as magnified nor widespread as they were at the start of the conflict. As sad as this entire situation truly is, and how devasting this has been to Ukraine and its people, we must set our emotions aside to effectively manage money. The hard reality of our occupation is that there are terrible things that happen in this world, and we must adapt to managing in all different types of economic and geopolitical environments.

As I wrote back in March (Russia/Ukraine and Fed/Interest Rates; How Quickly Things Can Change), when Ukraine was invaded on February 24th, the initial market reaction was down. In reviewing the market reaction to all the past geopolitical issues (either global or regional), the initial reaction is exactly the same; down. Why? Wars are shocks, and the market hates shocks. There is much uncertainly surrounding such horrible events. How long will this last? What will be the scope? Will other countries get involved? And, sadly, in this instance, Russia even postured about using nuclear force. So of course, the market went down. Rightfully so.

Yet, as time passes and more information is received, the market starts to trudge higher. You can see in this chart, that once we get 6 months removed from the start, market returns are positive 69% of the time. When we get out 12-Months, the market tends to be positive 83% of the time. The six-month post-invasion mark was August 24th, and the S&P 500 stood at 4140. This is -2% from where it was at the onset, 4225.

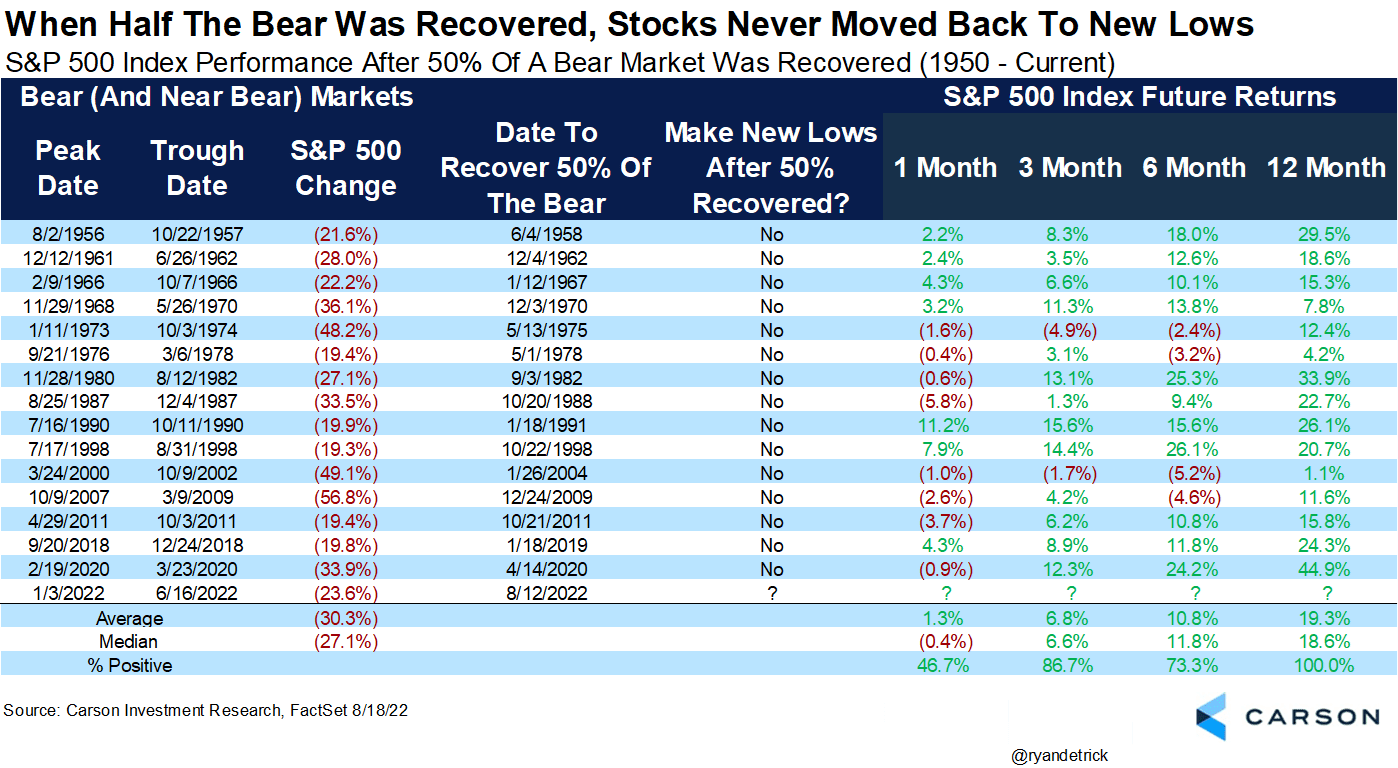

#4 The Market Rally Since June 16th

On June 16th, the S&P 500 closed at 3,666. This marked a -23.6% decline from the highpoint for the year (January 4th), and entered “bear market” territory. A bear market is broadly defined as when the market makes a -20% or greater move down. As of August 16th, the S&P sat at 4305, a whopping +17.4% rally from the June 16th low. This was a significant event because this means that the rally retraced over 50% of the decline. Quick math: -23.6% decline, a 50% retracement would be an upward move of +11.75%.

When Half of The Bear Market Was Recovered, Stocks Never Moved Back to New Lows (1950-now)

Now, let me clarify something here. There are myriad technical indicators and statistical anomalies that we can always dig up. Sometimes these indicators are right, other times wrong. We do not put pure faith into any indicators, because we feel it best to focus on what is going on with the specific companies we own for our clients. HOWEVER, the historical track record of this indicator was too juicy not to disclose. Take a look here.

{kind=link}

If history holds true, June 16th will have marked the lows. Indeed, it is a datapoint worth noting, but again, we never hang our hat on any single indicator. Besides, Mark Twain once had a famous quote: “History Never Repeats Itself, but It Does Often Rhyme.”

This discussion is not intended to be a forecast of future events and should not be considered a recommendation to buy or sell any security. Past performance is not indicative of future results. Investing involves risk. Principal loss is possible. Investing in smaller companies involves additional risks such as limited liquidity and greater volatility. No current or prospective client should assume that information referenced in this communication is a recommendation to buy or sell any security or is a substitute for personalized investment advice from your individual advisor. HCM does not provide tax or legal advice. Consult your tax or legal advisor for any related questions.

All information referenced herein is from sources believed to be reliable and is provided as general market commentary and does not constitute investment advice. This material was created for informational purposes only and the opinions expressed are solely those of HCM. HCM shall not in any way be liable for claims and makes no expressed or implied representations or warranties as to the accuracy or completeness of the data and other information. The data and information are provided as of the date referenced and are subject to change without notice.